Phosphate fertilizer trade flows change again

June 23rd, 2026 by Tom McIvor / Head of Phosphates, NPKs and Potash

June 23rd, 2026 by Tom McIvor / Head of Phosphates, NPKs and Potash

After years of reliance on Russian phosphate fertilizers, latest tariffs have largely moved Russian supply out of the EU ahead of another round of tariff additions from 1 July.

As recently as 2024, Russia held a 35% share of the EU’s import demand for phosphate fertilizers (2.0Mt out of 5.7Mt). Even in 2025, the EU imported 1.66Mt from Russia, a 30% share.

On top of existing duties of 6.5% against Russian product in the EU, a further specific fixed-rate duty has been applied since July 2025, which started at €45pt for phosphate fertilizers along with new CBAM import changes from the start of 2026.

From 1 July, the additional fixed rate duty on Russia rises to €70pt ($80pt), moving to €95pt in July 2027 and up to €430pt in July 2028.

While a limited decline was seen in 2025, imports from Russia in Q1 2026 to the region reached just 46,019t (6% of the total) from 442,846t in the same period 2025 (31% of the total) and as much as 57% market share in Q1 2022. A similar slump is reported in Q2 with stocks of Russian phosphate fertilizer in Europe now extremely low.

DAP/MAP imports by the EU from Russia in Q1 dropped to just 6% market share or 18,066t from 34% share in Q1 2024, according to latest TDM data, while NP/NPK imports saw a 93% volume drop to just 27,953t (a 7.6% market share from 44% in Q1 2025).

It is now likely that the EU’s phosphate fertilizer imports from Russia in the full year 2026 will drop to as low as 200,000t, or 6% of the expected 3.5Mt total, and should fall to near zero in 2027. Against last year this reflects a nearly 1.5Mt drop in volumes from Russia.

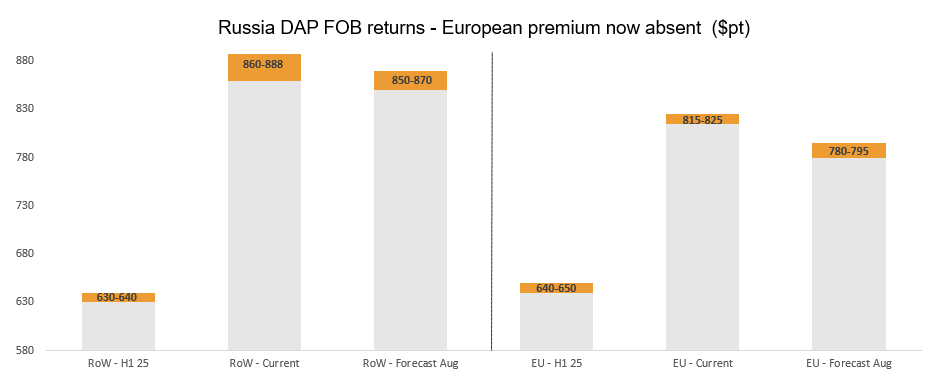

Instead, Russia’s supply to other markets – particularly Latin America, Africa and India – is expected to rise, with most of these markets moving to a premium for Russia against returns from Europe for the first time in 2026. Overall, Russian export supply may also be cut somewhat in 2026 due to lacking sulphur availability and increased drone strikes from Ukraine.

The EU supply decline in 2026 is being met by the region’s ongoing demand collapse on extremely weak affordability. The expected 3.5Mt import total for 2026 is the lowest in Profercy’s records and reflects a nearly 40% drop in import demand over the last two years.

While many had expected 2026 to see increased activity from North Africa, particularly to the EU, at this point there are no real winners from the reduced Russian supply. For instance, the EU’s imports from Morocco in Q1 dropped to 206,702t from 402,611t, moving OCP’s market share down to 27% from 28% in Q1 2025.

Moving forward into 2027 and 2028 as international phos ferts likely become more affordable and demand rises, OCP should still be the main beneficiary. Notably, however, Saudi Arabia entered the EU’s phosphate fertilizer market for the first time in Q1 2026, while other suppliers such as Norway, Egypt and Israel should also benefit.

Tom serves as Head of the Profercy Phosphates, NPKs and Potash coverage, overseeing price assessments, market analysis, and forecasting. To this role Tom brings over a decade of experience in fertilizer market research, price-portfolio development, and editorial commentary, combined with a background in financial journalism.

Tom McIvor

Head of Phosphates, NPKs and Potash

Provides you with our daily news and analysis, detailed weekly reports and price quotes

Sign Up Today