Potash affordability worsens as stocks rise in key markets

June 23rd, 2026 by Logan Collins / Senior Editor - Phosphates, NPKs & Potash

June 23rd, 2026 by Logan Collins / Senior Editor - Phosphates, NPKs & Potash

Potash affordability decreased 10% over the last month as falling crop prices met a relatively flat Profercy MOP import price index. Overall fertilizer affordability (including N and P in addition to K prices) has dipped 3.3% over the last month, as decreases in the affordability of DAP/MAP and MOP outweigh the improvements in affordability made by nitrogen products.

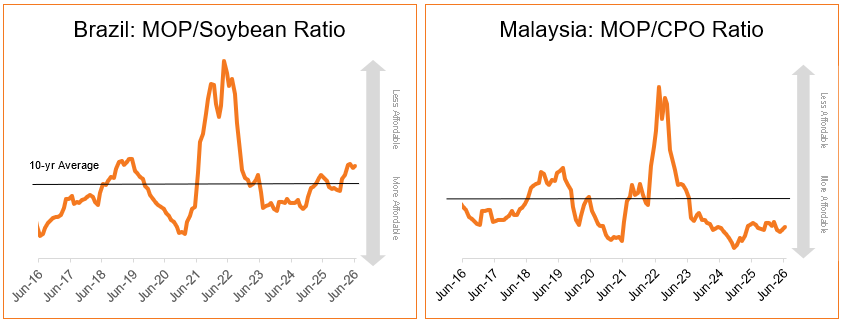

In Brazil, the Paranagua gMOP/soybean barter ratio as of 16 June at 16.6 increased on May due to lower soybean prices and flat MOP import prices. The April ratio was its highest level since November 2022 and is above its 10-year average of 14.3. This is a considerable decrease in affordability from this time last year, when the ratio stood at 15.1. The barter ratio is a measurement of the number of 50kg bags of soybeans required to purchase one tonne of MOP.

Likewise, in Southeast Asia, affordability has declined over the last month, with flat MOP prices meeting lower average palm oil prices. The MOP/CPO ratio is now at 35.03, up from 33.39 a month prior. This level is below the 36.98 ratio this time last year and is still far below the 10-yr average of 45.0.

Combined CBOT wheat, corn and soybeans prices are down 6.3% in the last month, with large decreases in corn and wheat accounting for the bulk of the decrease. Prior average CBOT gains were partly due to the ongoing crisis in the Middle East as well as adverse weather in Southeast Asia and the South Pacific caused by El Niño.

Worsening affordability relative to crop prices is likely to weigh on potash demand through the second half of 2026, especially as MOP stocks in some key consuming regions are also rising.

Brazil’s K2O stocks are estimated by Profercy to have increased 450-500,000t between the start of the year and early April to roughly 1.4-1.5Mt. Imports in the country are likely to slow through H2 as peak seasonal demand is met.

MOP inventories in China have also increased over the past month in line with seasonally lower consumption. The country's port inventories were estimated at 2.7-2.8Mt as of mid-June, up from around 2.2Mt one month ago. However, some reports have suggested further port inventory increases up to nearly 2.9Mt, which would be the highest volume seen since January 2025.

Worsening affordability and rising stocks are slightly bearish indicators for short-term potash prices, which have flattened over the past month in most key markets. Profercy's global MOP import price index has declined by $2pt since late May to $384.41pt.

Logan leads Profercy’s editorial coverage of the phosphates, NPKs and potash markets, delivering market‑focused analysis and price insight. With extensive experience covering global fertilizer markets, he brings expertise in trade flows, supply‑demand fundamentals and cost structures. Logan’s reporting helps subscribers understand key trends and make informed commercial decisions.

Logan Collins

Senior Editor - Phosphates, NPKs & Potash

Provides you with our daily news and analysis, detailed weekly reports and price quotes

Sign Up Today