Fall in US ammonia benchmark highlights bearish tone in the West, but East remains bullish on supply constraints

May 29th, 2026 by Richard Ewing / Head of Ammonia / Deputy Editor at Profercy Nitrogen

May 29th, 2026 by Richard Ewing / Head of Ammonia / Deputy Editor at Profercy Nitrogen

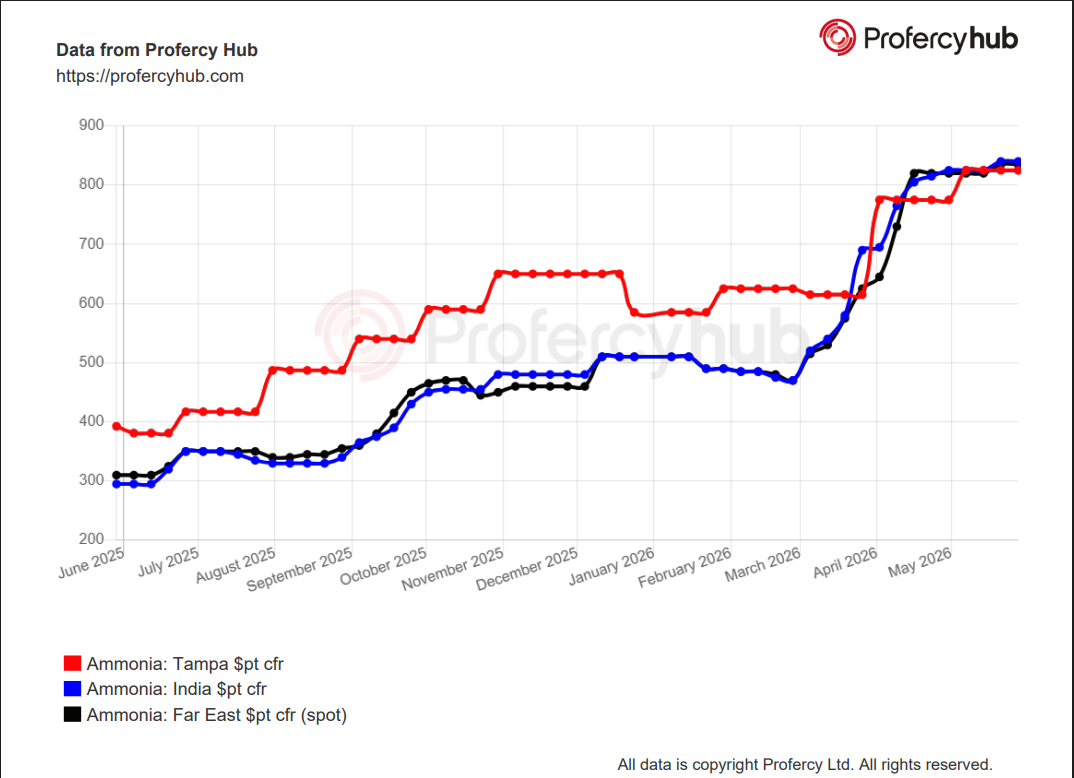

Today’s settlement of the Tampa contract for June loadings of ammonia at $775pt cfr, down $50pt from the May agreement, underlined the increasingly favourable supply scenario West of Suez, though the supply/demand balance is far tighter in the East due to the conflict in Iran.

News of the discount in the latest agreement between majors Yara and Mosaic was welcomed by leading buyers in the Americas and Europe, with the June settlement taking the key number back to April’s level.

While the size of the fall caught some by surprise, the downward trajectory had been expected in most quarters given the recent launch of major new export-oriented capacity in the US Gulf and a wave of production curtailments at phosphate manufacturers both sides of the Atlantic.

Ammonia plants across the Americas, including new units in Texas, are performing well and loadings in Algeria and the Baltic are occurring regularly, albeit small curtailments are heard elsewhere in North Africa.

At the same time, soaring sulphur costs have seen key phosphate manufacturers in Morocco, Brazil, Turkey and the US cut output, while prices of ammonia derivatives, especially urea and nitrates, have cooled over the past month.

Given the conflict-related loss of over 300,000t per month of Middle East material and the difficulty and cost of transiting the Strait of Hormuz, the picture is far more bullish in Asia Pacific, even though Iranian export availability is heard on the rise.

At least two Iranian spot cargoes were discharged in west coast India this week, with others expected to follow next month given one large producer closed three sales tenders in quick succession in May.

Also heading to Indian ports, albeit to terminals along the east coast, are several vessels that loaded in Southeast Asia and China in recent days.

Some of those cargoes are understood to comprise spot tonnes from traders, details of which should emerge in early June.

Indonesian export flows remain robust despite a lengthy turnaround at a major plant, while the restart of a large unit in Western Australia that fell quiet in late March has yet to be confirmed, with offshore material now on the water for two regular recipients of volume from that Yara facility.

Forecasting ammonia fertilizer markets requires deep familiarity with supply chains, energy dynamics and the shifting fundamentals that underpin global trade. Our team analyses every factor influencing ammonia prices — from feedstock costs and production changes to regional demand trends.

Our long-established forecasting approach is built on trusted data, extensive market relationships, and clear interpretation, enabling subscribers to cut through complexity with confidence.

As an ammonia specialist with over a decade of experience, I am proud to provide a service that uses forward-looking insight that is relied upon by major producers, importers, traders and financial institutions worldwide.

Richard Ewing

Head of Ammonia / Deputy Editor at Profercy Nitrogen

Provides you with our daily news and analysis, detailed weekly reports and price quotes

Sign Up Today