Ammonia prices firm on Middle East supply shock, though new US capacity cushions impact in West

March 20th, 2026 by Richard Ewing / Head of Ammonia / Deputy Editor at Profercy Nitrogen

March 20th, 2026 by Richard Ewing / Head of Ammonia / Deputy Editor at Profercy Nitrogen

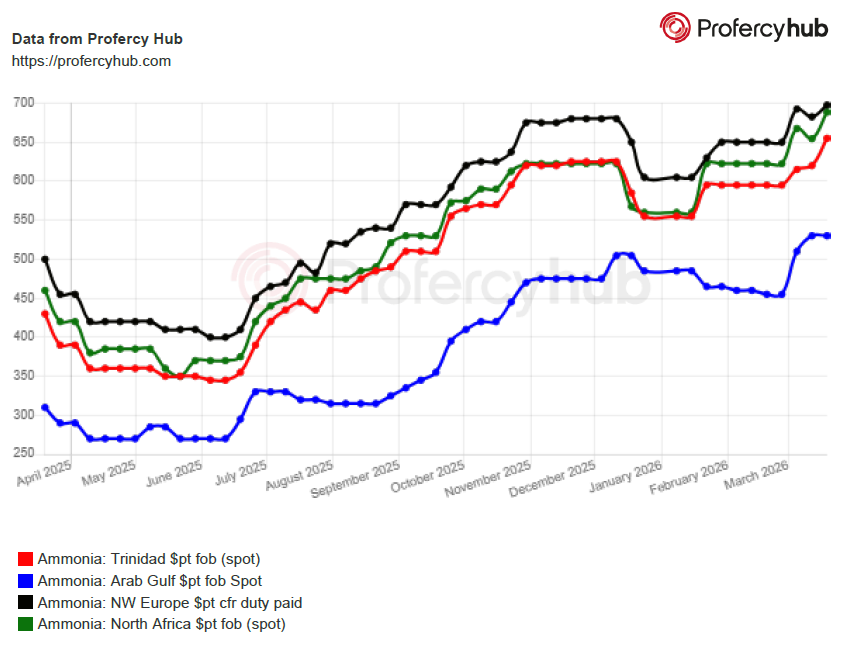

The fallout from the loss of a fifth of the world’s merchant ammonia volume continues to spread across international agricultural and industrial markets, with higher prices reported in all regions as suppliers scramble to source alternative cargoes.

Profercy data for 2025 ammonia shipments from the Middle East shows around 315,000t per month on average loaded at ports that require tankers to navigate the Strait of Hormuz.

Output from key export hubs in Saudi Arabia, Qatar and Iran has vanished since the start of the conflict through a combination of damage to upstream production facilities and vessels being unable to safely transit the vital waterway.

This just leaves Oman – which exported close to 45,000t per month on average last year – as the sole producer and supplier for now, with a 25,400t cargo about to head to west coast India.

The bulk of that volume was lifted from Salalah a few days ago by the Gas Ammon despite that port recently being closed for a few days due to damage from a missile strike that hit port infrastructure.

The balance is now under loading at Sur – around 1,000km north of Salalah – and supplier OQ Trading is understood to be planning to another delivery to India from the Sultanate before the end of the month.

With the taps almost turned off on supply from the Middle East, buyers and traders are increasingly looking for tonnes in Southeast and Northeast Asia, two regions that have enjoyed relatively abundant supply of late.

Chinese exports this January and February increased substantially year-on-year to around 125,000t from nearly 75,000t in the first two months of 2025, according to Profercy data.

Over the same period, Indonesian liftings – some of which went to domestic customers – came to nearly 300,000t, up 10% year-on-year. They included spot cargoes for Mexico, Morocco and Europe.

Leading producers and offtakers both there and in Malaysia are heard seeking up to $550pt fob (free on board) for April spot cargoes, an increase of 15-20% on last done.

Such a target suggests next spot business into India will be concluded above the $600pt cfr (cost and freight) threshold, especially given higher bunkering and insurance costs triggered by the Iran conflict have forced up freight rates worldwide.

Southeast Asia supply very healthy

Term material from Indonesia is currently heading to buyers in India and Northeast Asia, two regions that regularly receive Saudi contact cargoes from manufacturing majors Maaden and Sabic Agri-Nutrients.

Maaden had planned to load 200,000t this month, versus 155,000t in February and 100,000t in January, following the late January restart of one of its three 1.1m. tonne/year plants after several months of unscheduled maintenance.

However, only one of those plants is now heard to be running, albeit for phosphate production, with the other two units understood to be undergoing planned turnarounds that have been brought forward from later in the year.

Given the recent shortage of ammonia carriers, it would not be a surprise if Maaden was to let other players use some of its tankers until its vessels, most of which are outside the conflict zone, can return to load in the Kingdom.

In the West, the supply situation is in far better shape, with the first export cargo from Woodside Energy’s new 1.1m. tonne/year plant in Texas expected to comprise around 25,000t and to load as early as this weekend.

Together with the imminent return to operation of the Gulf Coast Ammonia (GCA) facility along the coast of the Lone Star state, the new capacity should help solve some of the headaches facing players exposed to the turmoil in the East.

Indeed, the only confirmed spot fob price this week – involving a 15,000t purchase by Trammo from Algeria’s Sorfert for April loading – came in slightly below the netback from a recent sale into Northwest Europe from Algeria by another player.

Trammo also sold cfr cargoes into the UK and Norway, with both deliveries originating from manufacturers in the Americas.

In addition, the supplier has been linked with a string of spot sales into Turkey from North Africa and Louisiana.

Buyers in Turkey busy in spot market

Turkish buyers were heavy users of Iranian ammonia prior to the conflict, with several vessels that performed those deliveries now sanctioned by US authorities.

However, Turkey remains a popular outlet for Russian material from the Baltic, although no new sales from there for Q2 arrival have yet been heard.

Assuming the healthy supply scenario in the West continues, price pressure is likely to be determined by capacity curtailments, if any, at European producers who are suffering from rising natgas costs.

Midweek natgas prices reflected $750pt ex-works for ammonia and $550pt ex-works for urea for an efficient plant. Those numbers exclude emissions costs.

The ex-works price for ammonia is roughly in line with latest offshore values, albeit buyers face the added cost hurdle of the European Union’s Carbon Border Adjustment Mechanism (CBAM) that came into force at the start of the year.

With further business for April and May expected to emerge by the end of this month, price direction is expected to remain divided along geographical lines for as long as the Middle East conflict continues.

However, the ammonia market is nothing but not resilient, with players having gained valuable experience of supply shocks amid the start of the ongoing conflict in Ukraine that removed around a fifth of the world’s merchant volume almost overnight.

By Richard Ewing

Head of Ammonia/Deputy Editor at Profercy

Forecasting ammonia fertilizer markets requires deep familiarity with supply chains, energy dynamics and the shifting fundamentals that underpin global trade. Our team analyses every factor influencing ammonia prices — from feedstock costs and production changes to regional demand trends.

Our long-established forecasting approach is built on trusted data, extensive market relationships, and clear interpretation, enabling subscribers to cut through complexity with confidence.

As an ammonia specialist with over a decade of experience, I am proud to provide a service that uses forward-looking insight that is relied upon by major producers, importers, traders and financial institutions worldwide.

Richard Ewing

Head of Ammonia / Deputy Editor at Profercy Nitrogen

Provides you with our daily news and analysis, detailed weekly reports and price quotes

Sign Up Today