Market Update: Urea values correct in wake of Indian Potash Limited tender

May 1st, 2026 by Chris Yearsley / CEO, Head of Nitrogen

May 1st, 2026 by Chris Yearsley / CEO, Head of Nitrogen

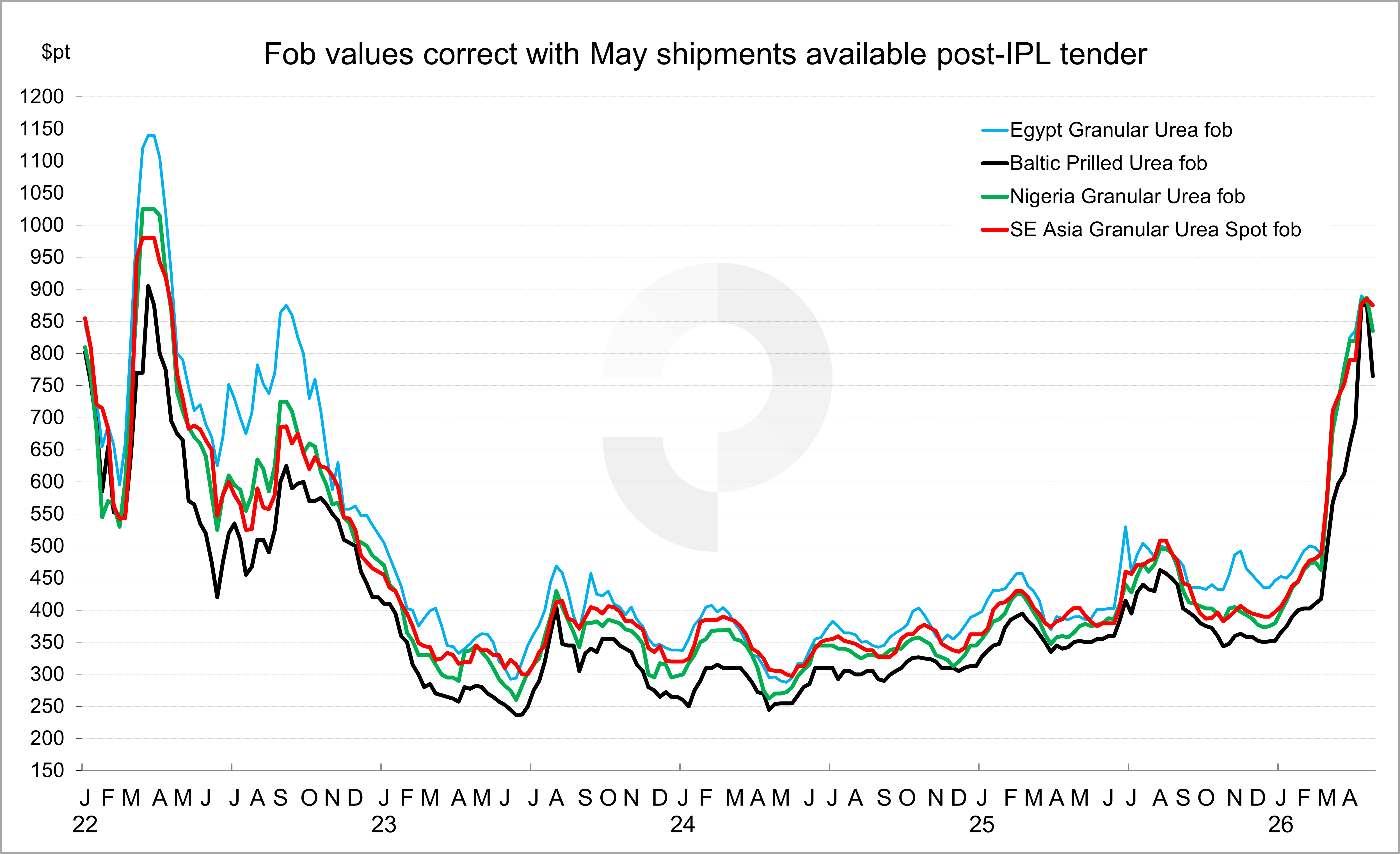

The market is on a softer footing, as a combination of affordability challenges, seasonality and available May shipments have weighed on global urea values.

Despite India lining up 2.5m. tonnes at multi-year price highs, a portion of which is still believed to be uncovered, spot cargoes have been on offer with buyers elsewhere unwilling to entertain Indian Potash Limited (IPL) tender premiums of $935pt cfr and above. Some participants have covered Indian business in the last week at significant discounts to implied netbacks.

The trend has been most pronounced in the west with product available in Algeria, Russia and Egypt, while re-export offers have also been circulating in Nola.

Central American buyers have managed to secure granular urea for the east coast in the low-$800s pt cfr. Offers in Brazil have declined to $770pt cfr with small volume business in Argentina taking place at marginally better values.

Fob offers in Algeria have declined to $830-850pt fob for large lots, with highest values sales in Egypt taking place in the mid-$800s pt fob for small volumes, some $35pt below earlier returns from India.

In the Baltic, prilled and granular urea offers have fallen into the $700s pt fob, a sharp decline on the $860-890pt fob levels previously achieved.

Returning to Nola, a combination of poor weather and sizeable March into April arrivals has weighed on local values. As such re-export business has been possible in the low to mid-$700s pt fob with sales concluded for Africa and Central America.

Eastern spot values have been more resilient with availability still impacted by the Middle East conflict and with China absent. Producers have maintained price ideas at, if not marginally below $900pt fob, albeit against no demand.

Supply may be heavily constrained, yet there has been no sense of urgency amongst importers. Global demand is often at a low-ebb in Q2 as US and European import demand wanes ahead of inquiry in Latam and India building through Q3. Further rounds of demand are, however, anticipated in Australia, while spot demand has been noted in Canada and Africa.

Market fortunes now look set to be dictated by events in the Middle East, the timing of further Indian inquiry and the potential for Chinese exports. For now, many buyers are maintaining a cautious, last-minute approach to procurement.

Originally published via the Profercy Nitrogen Service.

Forecasting Urea markets requires more than data, it demands experience, context, and an understanding of what truly drives change. From production costs and policy shifts to global trade balances, our team analyses every factor shaping the months and years ahead.

For over two decades, Profercy has refined a forecasting approach built on trusted data, deep fertilizer market relationships, and expert interpretation, helping our subscribers turn complexity into clarity.

We are proud to deliver forward-looking insights that guide some of the industry’s most important commercial decisions. Focused on providing clarity in uncertain markets - built on facts, experience, and decades of industry understanding.

Chris Yearsley

CEO, Head of Nitrogen

Provides you with our daily news and analysis, detailed weekly reports and price quotes

Sign Up Today