Ammonia prices start to soar as cuts at key production hubs begin to bite

March 27th, 2026 by Richard Ewing / Head of Ammonia / Deputy Editor at Profercy Nitrogen

March 27th, 2026 by Richard Ewing / Head of Ammonia / Deputy Editor at Profercy Nitrogen

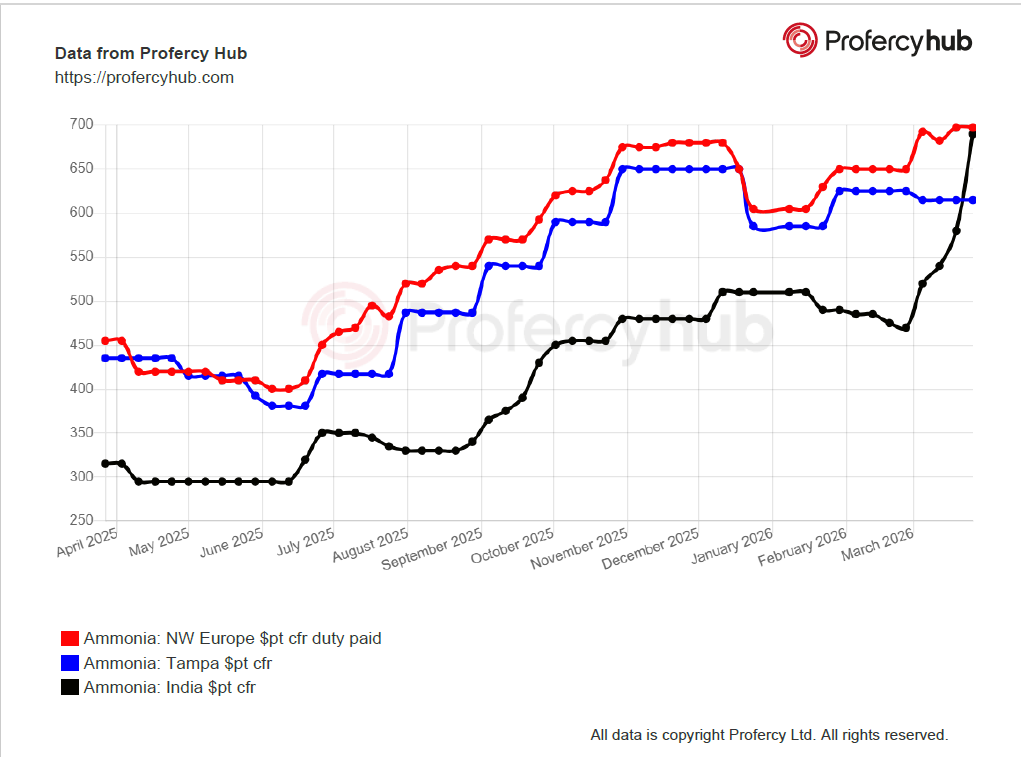

Today’s settlement of the Tampa contract for April loadings of ammonia at $775pt cfr, up an eye-catching $160pt from the March agreement, means the US benchmark is now within touching distance of a level not seen since early 2023.

The huge jump of over 25% in the key index comes amid the severe supply squeeze in the Middle East, with the conflict in Iran and surrounding region removing more than 315,000t per month from the merchant market indefinitely.

Unlike urea and nitrates markets, ammonia buyers had been spared some of the pricing pain due to robust supply in Northeast and Southeast Asia, but spot prices East of Suez are now rapidly increasingly as players scramble for replacement cargoes.

Adding fuel to the inflationary fire are capacity curtailments of 50% at some Algerian producers on feedstock cuts and the 4-6 week shutdown of Yara’s large Pilbara plant in Western Australia that leaves the Norwegian major short of 60-70,000t per month for local and foreign clients.

While plants in the Americas are understood to be performing well, cargoes from a pair of large new export-focused plants in Texas have yet to hit their stride but should start flowing regularly from early Q2.

Such major new capacity should apply the brakes to price rises in the West, albeit the Tampa settlement may yet breach the $790pt cfr seen three years ago – a level still way below the record $1,625pt cfr registered in April 2022 amid the early fallout from the war in Ukraine.

A crucial factor will be whether ammonia producers in Europe curtail capacity on rising natgas costs, though no major uptick in demand has yet been seen at leading import hubs across the continent.

With many market players in the West waiting for the Tampa settlement before kicking off talks over their next purchases, spot business is likely to be brisk next week, especially given the war in the Middle East shows little sign of de-escalating.

Indian buyers are likely to have to dig deep into their pockets to secure tonnes, with one spot buyer on the west coast – an area heavily reliant on Middle East material – receiving around 11,000t this week at a significant premium to last done.

Forecasting ammonia fertilizer markets requires deep familiarity with supply chains, energy dynamics and the shifting fundamentals that underpin global trade. Our team analyses every factor influencing ammonia prices — from feedstock costs and production changes to regional demand trends.

Our long-established forecasting approach is built on trusted data, extensive market relationships, and clear interpretation, enabling subscribers to cut through complexity with confidence.

As an ammonia specialist with over a decade of experience, I am proud to provide a service that uses forward-looking insight that is relied upon by major producers, importers, traders and financial institutions worldwide.

Richard Ewing

Head of Ammonia / Deputy Editor at Profercy Nitrogen

Provides you with our daily news and analysis, detailed weekly reports and price quotes

Sign Up Today