High Chinese backing prompts large India purchase, urea prices ease

July 8th, 2019 by Chris Yearsley / CEO, Head of Nitrogen

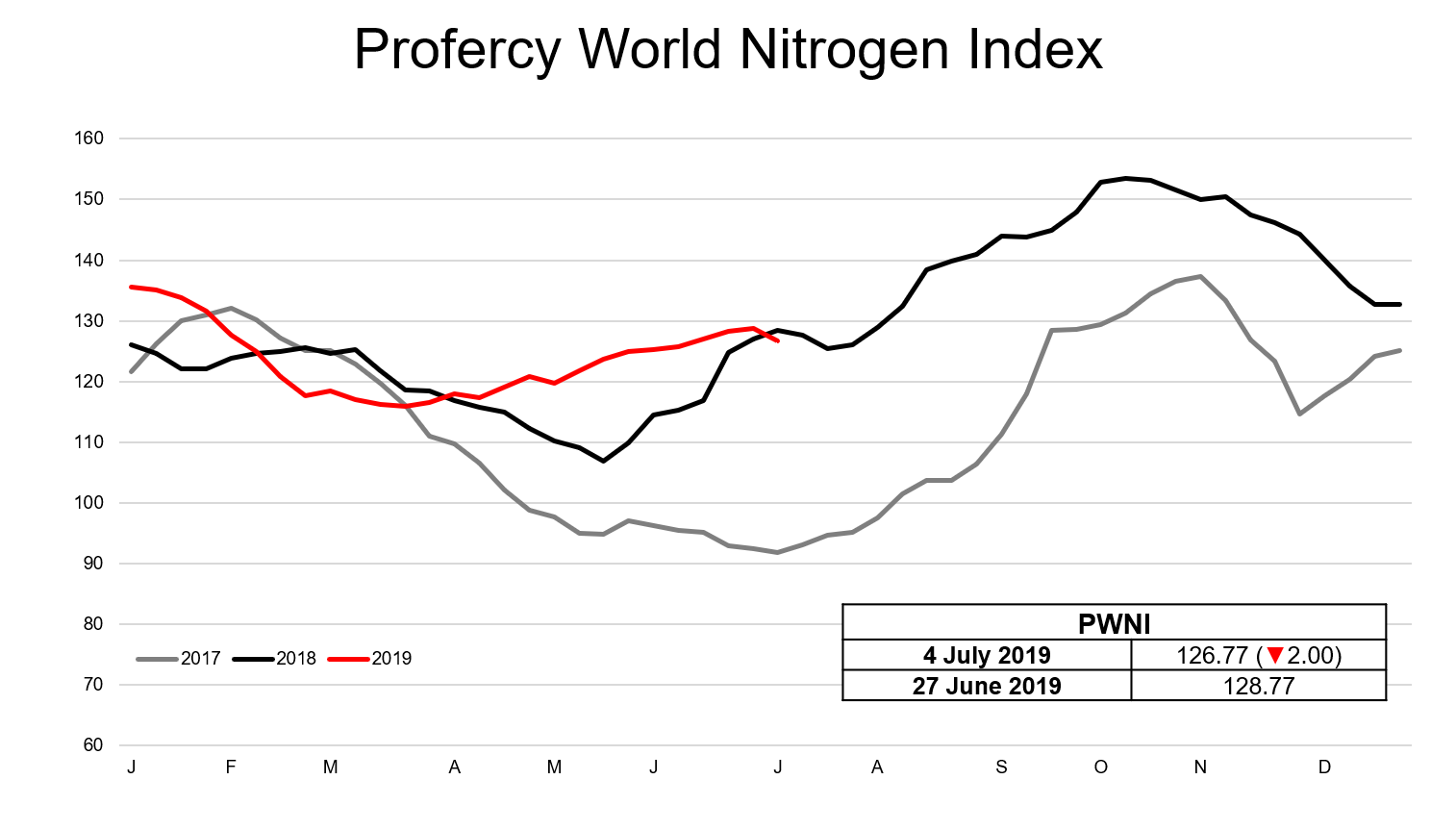

July 8th, 2019 by Chris Yearsley / CEO, Head of Nitrogen

While the announcement of an Indian urea purchasing tender on the 24 June was hardly a surprise, the results of the 1 July MMTC tender were anything but factored in. The first surprise was the price, lower than most in the market had anticipated. The second was the extent to which Chinese suppliers and traders were willing to back business into India. The third was the total volume booked by MMTC, just under 1.7m. tonnes, implying a possible lengthy absence before any future inquiry.

The lowest east coast offer was $292.63pt cfr Gangavaram with the lowest on the west coast at $295.97pt cfr. In the week running up to the tender conservative estimates put offer levels around $3pt or more above the eventual price. Indeed, many anticipated offers over $300pt cfr basis last done business in the Middle East at $285-290pt fob for July shipment.

The primary driver of lower offers was the availability of Chinese supply. Around 1m. tonnes have been committed to India by traders basis shipment from China at levels sub-$280pt fob. However, this has included significant short selling. Nevertheless, Chinese producers and traders have backed over 500,000-700,000t of business to date. This despite domestic prices for prilled urea reflecting around $290pt fob prior to the tender. Yet, a liquidity crunch in the domestic market has seen producers chase export business and encouraged domestic traders to short the local market.

The lower offer levels and higher availability prompted MMTC to substantially increase the volume it booked. Prior to the tender, around 1m. tonnes was widely anticipated to be targeted. In the end, MMTC booked 1.69m. tonnes. As noted above, the volume purchased increases the likelihood of a lengthy gap until the next Indian tender. Indeed, India bought 4.9m. tonnes under central tenders in the last April-March period. 2.8m. tonnes have been booked to date.

For this reason, a bearish mood was dominant in the market towards the end of last week. In the derivatives market, Middle East granular urea contracts for August traded sub-$275pt fob having traded at $290pt fob prior to the tender. Whether this sentiment persists will largely be shaped by the actual volumes made available from China. Should these fall short of expectations, or should Chinese nitrogen suppliers manage to raise prices, traders may be forced to look elsewhere for cargoes, including the Middle East, Egypt and the FSU.

By Michael Samueli, Nitrogen Market Reporter/Analyst

Forecasting Urea markets requires more than data, it demands experience, context, and an understanding of what truly drives change. From production costs and policy shifts to global trade balances, our team analyses every factor shaping the months and years ahead.

For over two decades, Profercy has refined a forecasting approach built on trusted data, deep fertilizer market relationships, and expert interpretation, helping our subscribers turn complexity into clarity.

We are proud to deliver forward-looking insights that guide some of the industry’s most important commercial decisions. Focused on providing clarity in uncertain markets - built on facts, experience, and decades of industry understanding.

Chris Yearsley

CEO, Head of Nitrogen

Provides you with our daily news and analysis, detailed weekly reports and price quotes

Sign Up Today