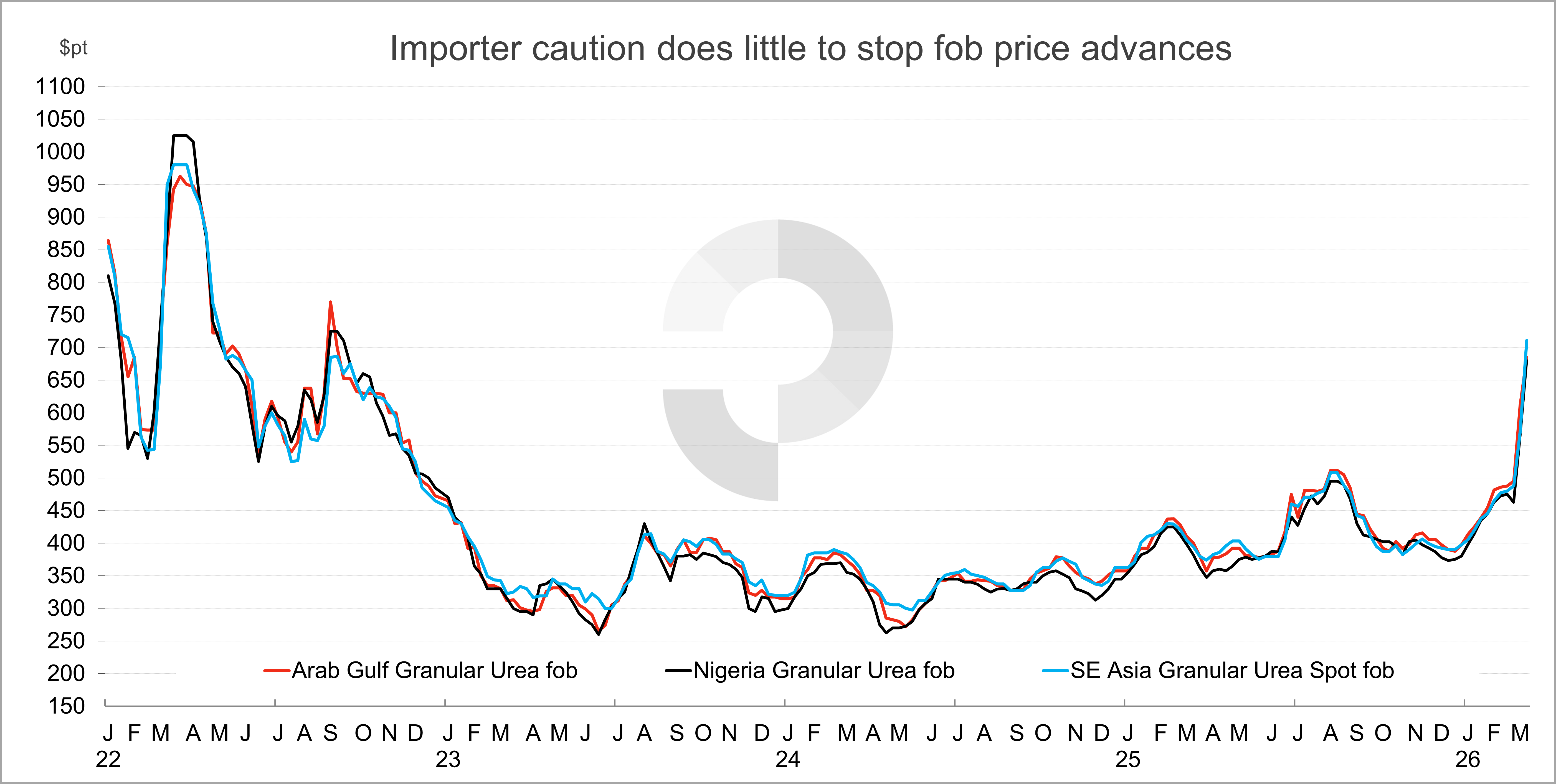

Middle East Crisis: Urea fob values maintain price advance despite buyer caution

March 13th, 2026 by Chris Yearsley / CEO, Head of Nitrogen

March 13th, 2026 by Chris Yearsley / CEO, Head of Nitrogen

The market is still reeling from the loss of supply from the Middle East, with this including shutdowns in Qatar and Iran, as well as the effective suspension of shipments from other suppliers north of the Strait. At presstime, the war was on its fourteenth day with vessels and ports still being hit by projectiles. Insurance and bunker costs are also presenting wider challenges for supply chains.

Assuming nameplate production rates, curtailments in the region, primarily in Iran, account for as much as 400,000t of lost product since 28 February. This does not include product stuck north of the Strait and unable to move.

For the time being, there have been no further reports of major production cutbacks in the UAE, Saudi Arabia and Bahrain, but concerns persist that inventory build-up will force tough decisions on producers. Such an event would significantly worsen supply woes.

Away from the Middle East, energy-induced challenges have been evident with Indian production rates under threat from gas feedstock constraints with these following curtailments in Pakistan and Bangladesh.

Crucially, lower operating rates in India look set to shape trade for April onwards cargoes with a fresh import inquiry widely anticipated. The status of 0.5m. tonnes lined up from the Middle East under the earlier RCF inquiry is in doubt.

Should India return, this will pit buyers elsewhere against one with comparatively deep pockets. To secure a large volume, India would have to draw material from suppliers east and west, including those in Africa, at the expense of other markets.

Fob values have unsurprisingly raced ahead of landed prices in most markets. Wide price differentials have been evident with Algerian fob values more than $100pt above cfr prices in the USA at one point in the past week.

The pace of price gains, alongside affordability and financing challenges, at a time when few are confident of how the Middle East crisis will play out has kept many on the sidelines. Those in Australia have been soliciting offers, while Canada, Colombia and parts of Europe have been active. US values firmed midweek.

Trade balances for March into April were already tight prior to latest developments. While the Strait is effectively blocked, buyers worldwide are in a difficult position with few easy options. With each day that passes, the stakes are getting higher.

Forecasting Urea markets requires more than data, it demands experience, context, and an understanding of what truly drives change. From production costs and policy shifts to global trade balances, our team analyses every factor shaping the months and years ahead.

For over two decades, Profercy has refined a forecasting approach built on trusted data, deep fertilizer market relationships, and expert interpretation, helping our subscribers turn complexity into clarity.

We are proud to deliver forward-looking insights that guide some of the industry’s most important commercial decisions. Focused on providing clarity in uncertain markets - built on facts, experience, and decades of industry understanding.

Chris Yearsley

CEO, Head of Nitrogen

Provides you with our daily news and analysis, detailed weekly reports and price quotes

Sign Up Today