India eyes $2.64bn urea award as tender lifts global fob values to four year highs

April 17th, 2026 by Chris Yearsley / CEO, Head of Nitrogen

April 17th, 2026 by Chris Yearsley / CEO, Head of Nitrogen

Indian Potash Limited (IPL) has a remarkable 2.8m. tonnes in hand through the 15 April tender, far exceeding volumes booked by India in previous tenders over the last five years.

While awards are still pending, participants expect India to secure the 2.5m. tonnes targeted in the tender, if not the full confirmed volume.

Should the latter materialise, the award value would surpass $2.64bn.

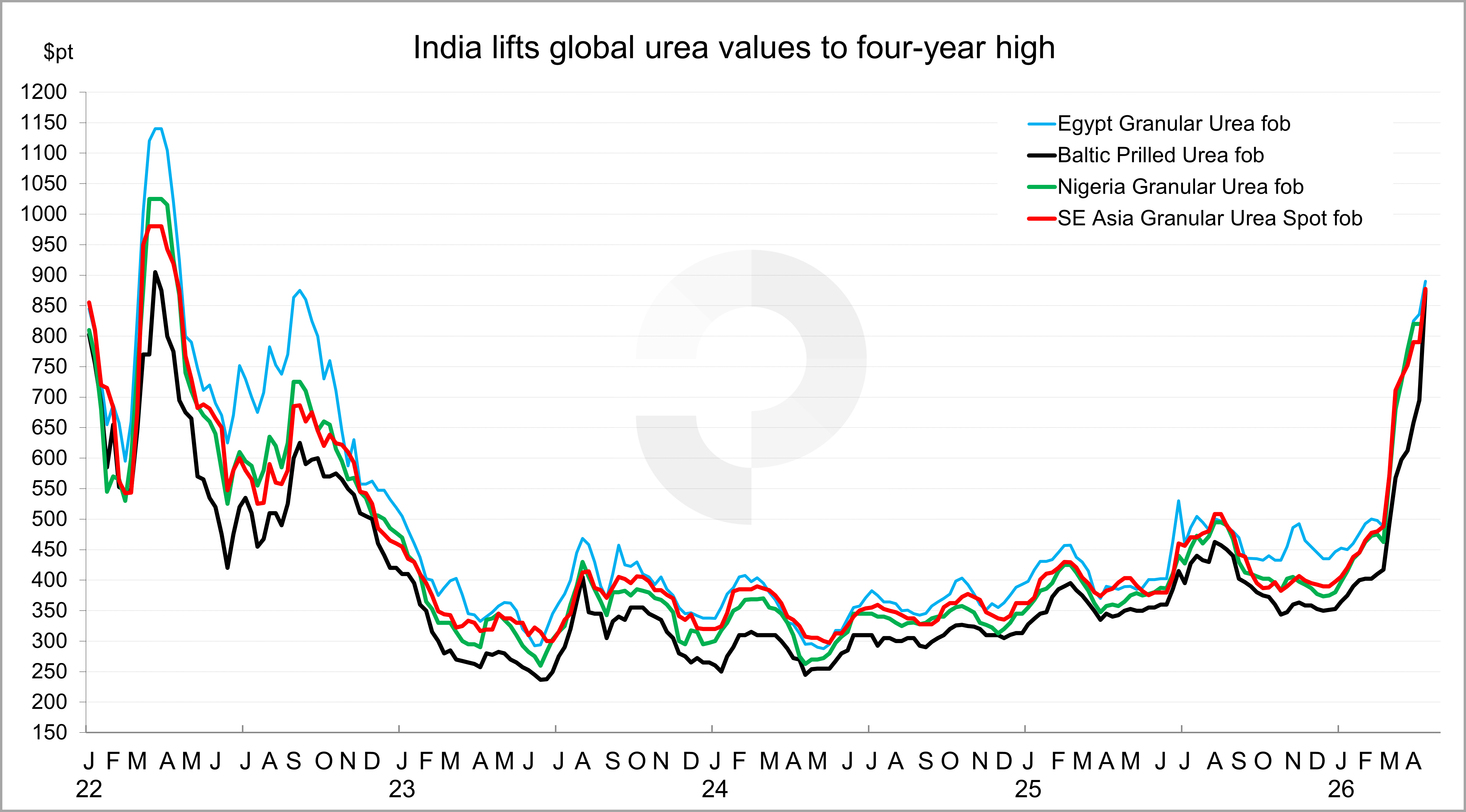

India's ability to secure such a substantial volume, well above earlier expectations on available supply given the Middle East-led supply crunch, has resulted from a lengthy shipment window to 14 June and the near-record level price on offer.

With this the first inquiry since the Middle East crisis began, the lowest offers were $427-447pt above those in the 18 February RCF tender. These were marginally below those in the 11 November 2021 inquiry which set a price record of $981.64-998.50pt cfr.

Just under 1.7m. tonnes have been confirmed at the west coast price of $935pt cfr, while 1.1m. tonnes are in hand on the east coast at $959pt cfr.

Widespread support from producers and other suppliers was anticipated given no other markets, bar Australia, have offered comparable returns.

For Russian producers, implied netbacks for granular urea are into the high-$800s pt fob Baltic, more than $160pt above realisable returns in the USA. For prilled urea, India offers an even greater premium given Latin American buyers have been unwilling to compete for volumes for several weeks.

With granular urea being confirmed to India, alongside prills, Russia stands to be the single largest supplier in the latest tender. Estimates of 800,000t or more are considered reasonable.

The situation is mirrored to varying degrees in Nigeria, Egypt and Algeria, with major volumes also lined up from SE Asia and Oman.

Re-export discussions have, unsurprisingly, been evident in many markets, including the USA. Basis lowest trading levels around $690ps ton fob Nola yesterday, cfr values in the US lag those in India $180-204pt. Some have also been heard exploring options in Brazil.

As is normal tender practice, IPL is expected to review confirmations and liaise with the Department of Fertilizers ahead of issuing awards. Participants in the tender expect IPL to award the full volume targeted, with some suggesting a greater volume purchase would be permitted.

The challenge facing other markets

Notwithstanding any surprises, the latest developments add to the difficulties facing buyers in many other markets. The market has been under significant pressure for some time owing to the extent of lost and blocked supply caused by the closure of the Strait of Hormuz at a time when China is absent from international urea trade.

Major importers and distributors in SE Asia and Australia would typically be sourcing urea for the current season for May through July arrival.

In the former, high international prices have paralysed many buyers for several weeks, while also encouraging switching to other products, such as amsul.

The extent of the supply squeeze in Australia has seen business concluded up to $950pt cfr equivalent for granular urea in the past week and news of government-backed deals for Indonesian product.

Prior to this, importers and distributors had been sourcing material from non-traditional suppliers, including those in Nigeria and Egypt.

This does not mean that buyers in offseason markets are unaffected. In Brazil, offseason arrivals are typically significant, allowing some degree of inventory building. Contract shipments from the Middle East, including Iran, have not been flowing, while other suppliers have focused their efforts elsewhere.

With global supply heavily constrained and producers now set to be comfortable through to first half June, buyers worldwide will now be hoping that a resumption of flows through the Strait of Hormuz can emerge. Any possible sign that China will re-enter the market towards the middle of the year would also be welcomed.

Forecasting Urea markets requires more than data, it demands experience, context, and an understanding of what truly drives change. From production costs and policy shifts to global trade balances, our team analyses every factor shaping the months and years ahead.

For over two decades, Profercy has refined a forecasting approach built on trusted data, deep fertilizer market relationships, and expert interpretation, helping our subscribers turn complexity into clarity.

We are proud to deliver forward-looking insights that guide some of the industry’s most important commercial decisions. Focused on providing clarity in uncertain markets - built on facts, experience, and decades of industry understanding.

Chris Yearsley

CEO, Head of Nitrogen

Provides you with our daily news and analysis, detailed weekly reports and price quotes

Sign Up Today