Urea markets firm: Chinese granular prices advance, Nitrogen Index up 3.29 points

August 1st, 2014 by Chris Yearsley / CEO, Head of Nitrogen

August 1st, 2014 by Chris Yearsley / CEO, Head of Nitrogen

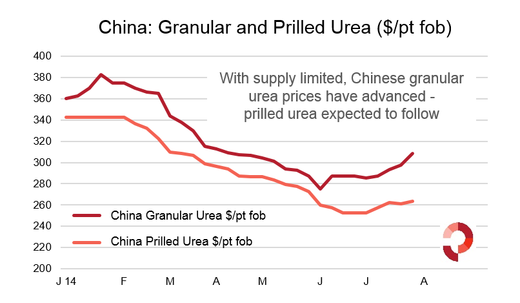

The trade balance assessment in our latest urea market forecast pointed to a tight urea market in the coming weeks. Indeed, the firmness in the market was evident this week with Chinese granular urea now offered at higher prices and with a modest price increase for September granular urea barges in the US. With little product available from major export origins for August, producers are also confident. The key question is now: how high can prices go?

As evidenced in the graph below, granular urea prices in China are well above those for prilled urea. This despite the efforts of producers who had targeted above $270pt fob China ahead of the recent Indian purchasing tender. In the West, prills are expected to fare better where they can compete as an alternative to the more expensive granular product in markets such as Brazil.

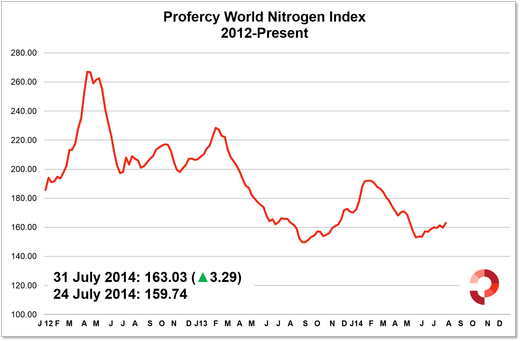

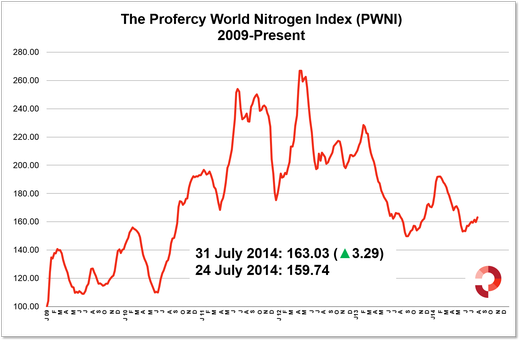

The PWNI is now at 163.09, up over 3 points on last week and regaining the ground lost by a temporary dip in US granular prices last week. Graphs charting the series since 2009 and 2012 are provided below.

[tabs][tab title="Profercy Nitrogen Index - 2012 Onwards"]

PWNI up 3.29 points as urea market firms.

PWNI up 3.29 points as urea market firms.

[/tab][tab title="Profercy Nitrogen Index - 2009 Onwards"]

PWNI up 3.29 points as urea market firms.

PWNI up 3.29 points as urea market firms.

[/tab][/tabs]

Further to our earlier blog entry on Indian urea subsidies, sources in India indicate that the new Government is reviewing a number of policy options with a desire to increase Indian domestic urea production. It has been suggested that officials are keen to see an increase in domestic production of 2 million tonnes by 2015 and 5 million tonnes by 2017. The drive is intended to reduce India’s reliance on foreign urea, and in particular on purchasing through public tenders. The current import requirement is 8m. tonnes.

Proposals under consideration include plans to reimburse producers reliant on imported LNG feedstock with any subsidy covering the cost difference between $8.2mmBtu and a maximum price just short of $20mmBtu. It is of course early days as the new Government considers its options, but the debate is worth following given the significance of Indian demand to prilled urea suppliers in the East.

The Profercy World Nitrogen Index is published every week and is based on price ranges provided by the Profercy Nitrogen Service. This includes prilled and granular urea, UAN, AN, ammonium sulphate and ammonia. A full methodology can be found here.

Profercy's Nitrogen Service includes daily news, weekly analysis and monthly forecast reports. For more detailed information on specific products and individual markets, please sign up for a free trial or for more information on the Profercy Nitrogen Service, please click here.

Forecasting Urea markets requires more than data, it demands experience, context, and an understanding of what truly drives change. From production costs and policy shifts to global trade balances, our team analyses every factor shaping the months and years ahead.

For over two decades, Profercy has refined a forecasting approach built on trusted data, deep fertilizer market relationships, and expert interpretation, helping our subscribers turn complexity into clarity.

We are proud to deliver forward-looking insights that guide some of the industry’s most important commercial decisions. Focused on providing clarity in uncertain markets - built on facts, experience, and decades of industry understanding.

Chris Yearsley

CEO, Head of Nitrogen

Provides you with our daily news and analysis, detailed weekly reports and price quotes

Sign Up Today